Original article from US News & World Report, July 9, 2020

According to a late June 2020 survey from U.S. News & World Report, the COVID-19 pandemic has left more than four in 10 Americans worried about money. An additional 27% say they aren’t worried about money, but they still feel the need to be cautious with their spending.

Other survey results uncovered one of the possible sources of anxiety. When asked how long their emergency fund would cover their expenses, almost 37% of survey respondents say they don’t even have an emergency fund. And close to 10% say they could only cover expenses for one month.

There was a time, back in my 20s, when I didn’t have an emergency fund. I can tell you from personal experience that having a zero balance in your rainy-day fund makes it hard to sleep at night. But a lack of savings isn’t the only thing worrying consumers these days.

There was a time, back in my 20s, when I didn’t have an emergency fund. I can tell you from personal experience that having a zero balance in your rainy-day fund makes it hard to sleep at night. But a lack of savings isn’t the only thing worrying consumers these days.

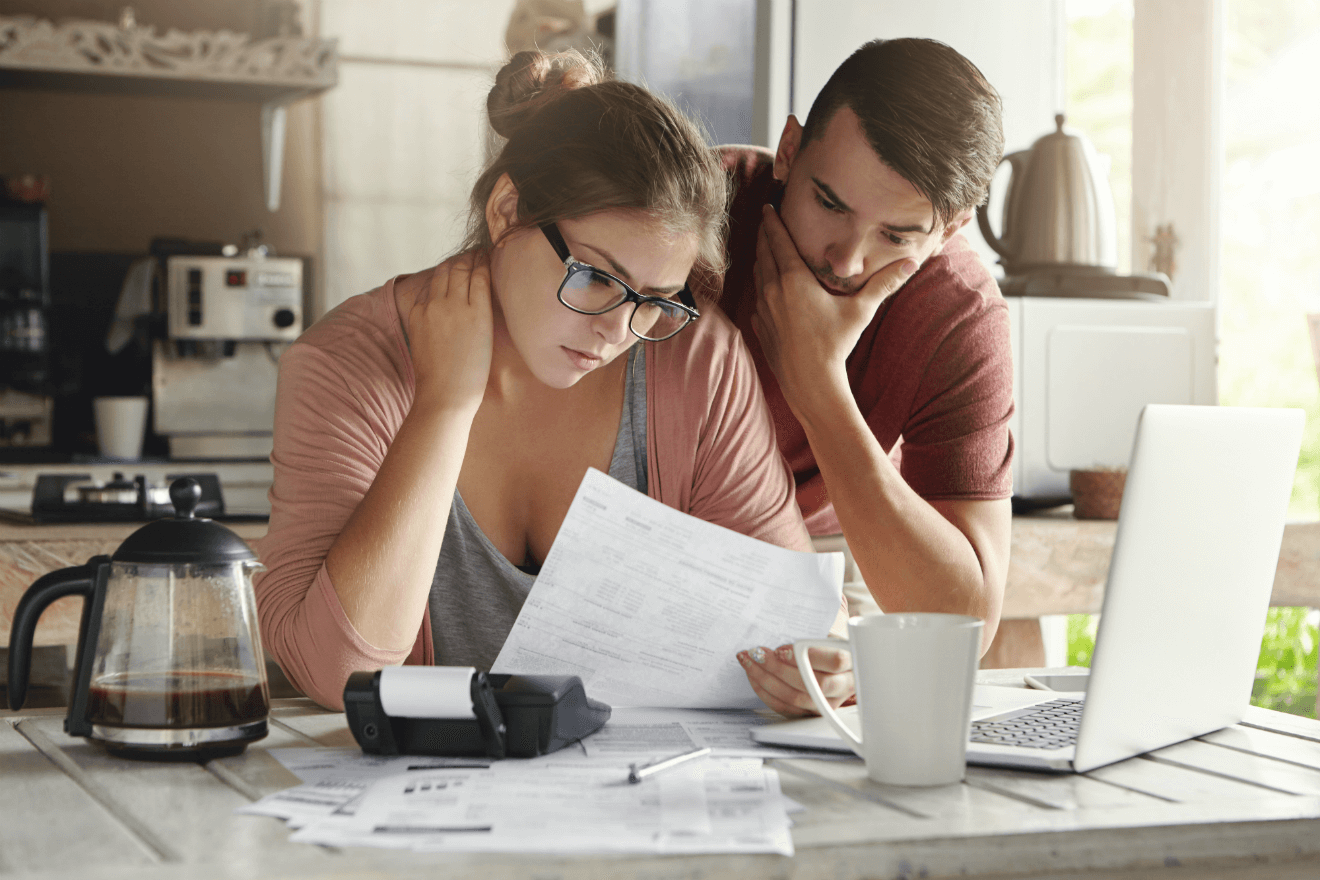

What Are Americans Stressed About?

Although the state of the economy was pretty grim in April and most of May, things got better after businesses started reopening. But even if your personal finances are improving, we all know we’re not out of the woods yet with COVID-19.

We’re still recovering emotionally from the impact of the lockdowns on our personal finances. For instance, the average 401(k) balance dropped almost 20% in March – and that was just the beginning of the crisis. Investments are bouncing back, but it takes time.

Here are some sources of stress identified by respondents:

- More than 25% are stressed about their shrinking savings and investments.

- About 21% worry about keeping up with bill payments.

- Around 21% are anxious about job security.

- Nearly 17% are worried about rising personal debt.

And adding to the list of worries is that provisions of the Coronavirus Aid, Relief and Economic Security Act are set to expire on July 31. More than 9% of respondents say they’re stressed about expiring relief options. When respondents were asked if they’re worried about losing the extra $600 weekly in federally funded unemployment benefits, 15% said yes.

The CARES Act also allowed consumers to defer mortgage and student loan payments. With the law set to expire soon and uncertainty about the next relief bill, 8% are worried about being able to cover their deferred payments.

How to Build an Emergency Fund During a Pandemic

The results did show some good news, though. A solid 29% of consumers say they can cover expenses for at least six months. When you have a strong emergency fund, you’re less likely to fret when a crisis hits because you have some time to figure out what to do.

I don’t care if you have to start with $20; just get started. How much money do you need in your emergency fund? I recommend working on your fund until you can cover at least six months of expenses. But set a one-month goal for starters and work your way up.

I know this isn’t the easiest time to build your savings, but it can be done with a little creativity, boldness and persistence.

So, let’s start brainstorming. Here are just a few suggestions for finding money during dark times.

Ask for money.

I thought I’d start with the easiest way to get money – from other people. Let everyone know you want cash for birthdays and holidays. Set up a Venmo account or something similar to make receiving payments easy. Make sure the gift goes into your new savings account.

Ask for a raise.

No, this isn’t crazy right now. If you’re in an industry that’s doing well, get what you’re worth. Clearly, if you’re in the travel industry, for example, this is probably not a valid strategy. But do keep it in mind for the future.

Save your tax refund.

If you’re due for a refund, consider this a windfall. Unless you’re carrying high-interest credit card debt, put the entire amount in your emergency fund.

And when life calms down, look at your withholding amounts with your employer. Ideally, you want access to the cash during the year to increase your cash flow. When you get a large refund, you’ve been giving the government an interest-free loan.

Get a side hustle.

Earning extra money on the side for six months or so is a perfect way to increase your cash flow temporarily. A good example is working a second job during the holiday season.

A side gig is more difficult to pull off if you have a family or a full-time demanding job, but it’s not impossible. Focus on finding work that you can do at home so you aren’t spending precious time in traffic.

Track your expenses.

Do this for a month, and you’ll be amazed at where your money is going, especially if you’ve given in to the lure of online shopping.

Again, think in terms of temporary measures. You don’t have to eliminate everything you enjoy. Just cut back on unnecessary expenses until you have a healthy rainy-day fund.

Use a rewards credit card.

This might seem counter-intuitive, but there’s a benefit to this. A credit card with cash back on everyday items, like groceries, means rewards can add up and be used as a statement credit. But most consumers aren’t taking advantage of this opportunity. A recent U.S. News survey, also taken in June 2020, about consumers’ grocery-buying habits showed that more than 39% of respondents pay for groceries with a debit card.

Using a cash back card allows you to spend less on essential expenses. Many of these cash back cards don’t have annual fees, and some also come with sign-up bonuses, which gives you an extra infusion of cash. Take the extra cash you have left over after you pay grocery expenses and put it in your new emergency fund.

Another Way to Reduce Anxiety? Maintain a Good Credit Score

A great credit score helps you save money in many areas of your life. This might not directly add cash to your savings account, but it helps you maintain a lower-cost lifestyle. Believe me, you can save thousands, for instance, over the life of a mortgage if you qualify for the best rates.

The survey showed that almost half of respondents don’t know whether their credit score has changed since the pandemic began. Always know where your credit stands just in case you need a personal loan to financially survive an emergency.

As 2020 has shown us, life is wildly unpredictable. Having good credit at least reduces your odds of needing a high-interest loan to survive a crisis. Just knowing that this is an option can reduce your financial anxiety.